▸ Trading Psychology · The Math

The Win-Rate Fallacy

Ask a struggling trader how they’re doing and they’ll tell you a percentage. “I’m right about 65% of the time.” It sounds like a report card, and it feels like the number that matters. It isn’t. Win rate is the most quoted and most misleading statistic in trading — a vanity metric that tells you how often you’re right and nothing about whether you’re making money. You can win 70% of your trades and go broke. You can win 35% and get rich. Here’s the math that proves it, and why chasing a high win rate is one of the most expensive habits you can build.

What win rate actually measures (and what it doesn’t)

Win rate is simple: the percentage of your trades that close in profit. Fifty-five wins out of a hundred trades is a 55% win rate. The calculation is easy, which is exactly why people over-trust it — it feels precise. But it measures only how often you’re right, never how much you win when you’re right or lose when you’re wrong. That single omission is the whole problem: a strategy can have a glittering win rate and still bleed money, and a strategy that loses more often than it wins can compound a fortune. (HeyGoTrade: win rate measures frequency, not magnitude)

The reason this matters so much is behavioral. Human beings are wired to want to be right, and a high win rate scratches that itch directly — every green trade is a little hit of “I was correct.” Profitability doesn’t feel like anything in the moment; it only shows up in the account over time. So traders optimize the variable that feels good (accuracy) instead of the one that pays (expectancy), and the two are only weakly correlated. Winning 70 of 100 trades can still lose money; winning 35 of 100 can still make it. (JournalPlus: we optimize feeling right over being profitable)

The number that actually pays you: expectancy

The metric that matters collapses both halves — how often and how much — into one figure: expectancy, the average amount you make or lose per trade. The formula is (win rate × average win) minus (loss rate × average loss). Positive means your approach has a mathematical edge; negative means it doesn’t, and no win rate can save it. Think of it as batting average versus runs scored: a player who bats .250 with home runs outscores one who bats .350 with nothing but singles. Expectancy is the runs. (The Trapped Trader: expectancy is the runs scored)

Here’s the classic trap made concrete. A trader wins 70% of the time, banking $150 on each winner but losing $400 on each loser. Feels like a winner — right seven times out of ten. Run the math: (0.70 × $150) minus (0.30 × $400) equals a negative expectancy of −$15 per trade. With a 70% win rate, the more they trade, the more they lose. Cut those losses to $200 and the same 70% win rate flips to +$45 a trade. Nothing about their accuracy changed. Only the size of the losses did. (Trademetria: the 70% win rate that loses money)

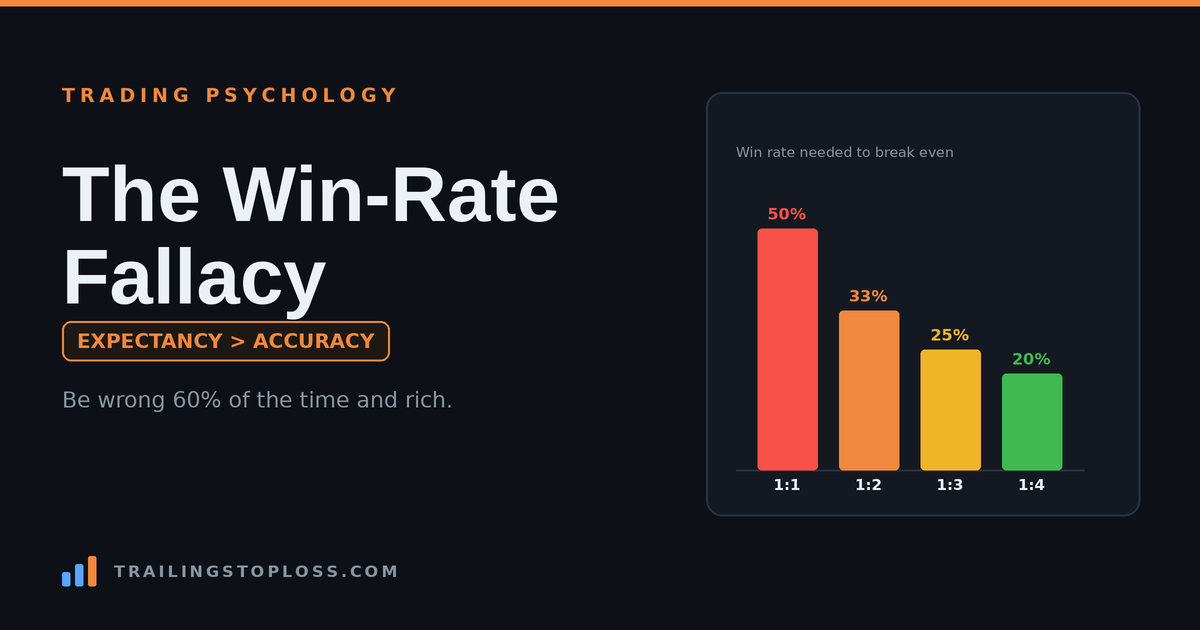

The break-even win rate

Every risk-reward ratio has a win rate you must clear just to break even — and it’s lower than most traders think. The formula is clean: break-even win rate = 1 ÷ (1 + your reward-to-risk ratio). At 1:1, you need to win 50% of the time. At 1:2, only 33.3%. At 1:3, just 25%. The moment your winners are bigger than your losers, the bar for profitability drops below a coin flip — which is why “being wrong most of the time” is a perfectly viable, even professional, way to trade. (Trader’s Second Brain: break-even win rate = 1/(1+R:R))

Watch a 40% win rate beat a 70% one

This is the comparison that should permanently rewire how you read your own stats. Two traders, same 10 trades’ worth of math, wildly different accuracy — and the less accurate one wins. (Trader’s Second Brain: 40% at 3:1 beats 70% at 1:1)

| Trader | Win rate | Reward : risk | Expectancy per trade |

|---|---|---|---|

| “Feels like a winner” | 70% | 1 : 1 | (0.70 × $1) − (0.30 × $1) = +$0.40 |

| “Wrong most of the time” | 40% | 3 : 1 | (0.40 × $3) − (0.60 × $1) = +$0.60 |

| The vanity trap | 70% | 1 : 0.25 | (0.70 × $0.25) − (0.30 × $1) = −$0.125 |

The 40%-win-rate trader makes 50% more per trade than the 70% one — and the 70% trader who cuts winners tiny to protect that shiny accuracy is quietly losing money on every trade. Many consistently profitable traders sit in the 35–50% win-rate range, because their average winner dwarfs their average loser. Trend followers routinely win a third of the time and build serious wealth, precisely because they let winners run three to five times their risk while cutting losers at −1R. Their edge was never accuracy. (JournalPlus: the edge is asymmetry, not accuracy)

Why chasing win rate actively destroys your edge

Here’s the part that makes this a psychology problem and not just a math lesson. The moment you decide “being right” is the goal, you start doing specific, measurable things that wreck your expectancy. You cut winners short to lock in the green and pump your win count. You widen stops to avoid booking a loss. You take lower-quality setups just to add another tick to the tally. Every one of those moves shrinks your average win and inflates your average loss — the exact two levers that determine whether you make money. Chasing the number that feels good sabotages the number that pays. (TradeZella: chasing win rate tanks expectancy)

You’ll recognize the two big ones from elsewhere on this site: cutting winners short and widening stops are the disposition effect and the break-even-stop reflex in action — and the hidden motive behind both is often just protecting a win-rate number. Loss aversion tells you a booked loss hurts twice as much as a booked win feels good, so you contort your entire exit strategy to avoid the sting, and the win rate goes up while the account goes down. The vanity metric isn’t just useless; it’s the bait that leads you into every other exit mistake. (Zaye Capital: loss aversion makes low win rates feel unbearable)

What to track instead

Win rate isn’t worthless — it’s just a diagnostic, not a target. Here’s how to use it correctly and what to watch instead. (TradeZella: use win rate for consistency, not as a target)

- Lead with expectancy. Calculate (win rate × avg win) − (loss rate × avg loss) from your journal. If it’s positive, you have an edge; if it’s negative, no amount of “being right more” fixes it. This is the number that decides whether trading pays you.

- Use profit factor as your one-glance sanity check. Gross profit ÷ gross loss. Below 1.0 is a losing system; 1.2–1.5 is a tradeable edge (roughly prop-firm minimum territory — FTMO’s challenge floor sits around a 1.2 profit factor); above 2.0 is either genuine skill or small-sample noise, so keep testing.

- Measure your realized R:R, not your planned one. Many traders plan 1:3 and actually average 1:1.4 because they keep exiting winners early. The gap between the two is the money your win-rate obsession is costing you, in plain numbers.

- Treat win rate as a consistency alarm. If you normally run 45% and it suddenly drops to 30%, something broke in your setup process. If it jumps to 65%, you may be taking lower-quality signals to chase the number. Stability matters; the specific figure doesn’t.

- Demand a real sample. Expectancy from 10–15 trades is almost meaningless — randomness dominates. Aim for 30 trades minimum to compute it, 100+ before you trust it, and recalculate periodically as conditions change.

🧠 The one line to rememberWin rate is vanity. Expectancy is sanity. The traders quietly compounding accounts aren’t the ones who are right most often — they’re the ones who’ve built a system where being right simply matters less than the math working. Stop asking “was I right?” Start asking “what’s my expectancy?”

The bottom line

A high win rate feels like proof you’re good at this. Often it’s proof of the opposite — that you’re cutting winners and dodging losses to protect a number that doesn’t pay. Roughly 70–80% of active day traders lose money over any given year, and plenty of them have perfectly respectable win rates; what they lack is positive expectancy. Flip the question. Stop counting how often you’re right and start measuring how much your rightness is worth, because the market pays in dollars, not in accuracy. Be wrong 60% of the time and rich. It’s allowed. (JournalPlus: Barber & Odean — most active day traders lose)

Put the math to work: model your edge with the win-rate & expectancy calculator, map reward-to-risk before you enter on the Stop-Loss & R:R Visualizer, and log realized R-multiples on the P&L Calendar. This piece is part of our trading psychology guide — the vanity-metric trap connects straight to cutting winners and riding losers.

FAQ

Can a low win rate still be profitable?

Yes — easily. Profitability depends on expectancy, not accuracy. A 40% win rate at 3:1 reward-to-risk has an expectancy of (0.40 × 3) − (0.60 × 1) = +0.60R per trade, solidly profitable despite losing 60% of the time. Many trend-following traders win only 30–40% of trades and compound serious returns because their winners dwarf their losers.

What is a good win rate in trading?

There’s no universal number — it depends entirely on your reward-to-risk ratio. A scalper might need 55–65%; a trend follower thrives at 30–40%. The right question isn’t “what’s a good win rate?” but “is my win rate high enough to be profitable at my R:R?” Break-even win rate = 1 ÷ (1 + R:R), so at 1:3 you only need to clear 25%.

What is expectancy and how do I calculate it?

Expectancy is the average profit or loss per trade: (win rate × average win) − (loss rate × average loss). Positive means your system has a mathematical edge; negative means it doesn’t, regardless of win rate. It’s the single most important number in trading because it combines how often you win with how much — the two things win rate alone ignores.

Why do I lose money even though I win most of my trades?

Almost always because your average loss is bigger than your average win. If you cut winners early and let losers run (or widen stops), you can win 70% of trades and still have negative expectancy — e.g. banking $150 per win but losing $400 per loss is −$15 per trade. Fixing the size of your losses, not the frequency of your wins, is the cure.

Should I try to improve my win rate?

Only if you can do it without shrinking your average win or enlarging your average loss — which is hard, because most win-rate-boosting habits (cutting winners early, widening stops, taking marginal setups) actively lower expectancy. Improve expectancy and profit factor instead. Use win rate as a consistency alarm: sudden changes signal a broken process, not a target to chase.

TrailingStopLoss publishes independent, funded-trader analysis of prop firms, strategy, and trading psychology. Educational content only — not financial advice. Trading futures involves substantial risk of loss.