Post-Market Briefing — Wednesday, May 20, 2026

Stocks Rip Higher Into Nvidia's Print, Bonds Catch a Bid, and Everyone Pretends They Were Bullish All Along

After three sessions of getting their teeth kicked in by the bond market, equity bulls woke up Wednesday, drank an espresso, and decided rising yields were yesterday's problem. The Dow climbed back above 50,000, the Nasdaq jumped over 1.5%, and oil quietly slipped under $100 for the first time in weeks as traders priced in the possibility that Washington and Tehran might actually stop shooting at each other. Then, after the bell, the main event arrived: Nvidia delivered another monster quarter that briefly sent its stock down 2% — because at this point, beating estimates by $2 billion is apparently a disappointment.

Closing Scoreboard

| Index / Asset | Close | Day Change |

|---|---|---|

| S&P 500 | ~7,433 | +1.08% |

| Nasdaq Composite | — | +1.54% |

| Dow Jones Industrial Avg | ~50,000+ | +1.31% |

| WTI Crude | ~$100 | −2nd straight session |

| 10-Year Treasury Yield | ~4.61% | Modestly lower |

| Gold (spot) | $4,503 | +0.34% |

| Silver (spot) | ~$75 | +1.7% |

| Bitcoin | ~$77,330 | +0.55% |

| Ethereum | ~$2,133 | +0.90% |

Equities: The Bounce Nobody Asked For (But Everyone Took)

Wednesday was the kind of session that rewards people who don't check their phones. After three consecutive down days, the major indexes ripped higher, with the Nasdaq leading the charge on tech enthusiasm and pre-Nvidia positioning. The Dow gained 1.31% and reclaimed the 50,000 level, the S&P 500 added 1.08%, and the Nasdaq surged 1.54%. Discretionary (+2.39%) and Technology (+2.11%) led the sector tape, while Energy (−2.08%), Staples (−0.52%), and Health Care (−0.07%) were the only decliners as oil prices retreated and rotation pulled money out of defensives, per TheStreet's market wrap.

The driver here is mostly about what didn't happen. Treasury yields, which had punched through 52-week highs on Monday with the 10Y at 4.657%, the 20Y at 5.189%, and the 30Y at 5.171%, finally took a breather. The 10Y settled around 4.61%, giving equity multiples some room to breathe and triggering the kind of broad-based bid that suggests systematic flows and short-covering did a lot of the heavy lifting. If you're trading the indexes, this is exactly the kind of session that traps both sides — bulls feel vindicated, bears feel ambushed, and nobody learned anything useful. For more on how rate moves translate to your day trading setups, the relationship between long-end yields and tech multiples remains the cleanest macro signal on the tape, according to CNBC.

Futures Markets: Oil Cracks, Equity Futures Front-Run the Bounce

Crude was the headline futures story. WTI fell for a second straight session to around $100 per barrel as traders grew cautiously optimistic that Washington and Tehran could reach an agreement — despite Trump simultaneously warning he could "resume strikes if negotiations fail." Nothing says "cautious optimism" like a president threatening airstrikes from one side of his mouth while saying the conflict could end "very quickly" from the other. Brent and WTI have been trading with an inflated risk premium since the Strait of Hormuz closed, and any meaningful sign of de-escalation pulls that premium right back out, as reported by Trading Economics.

Equity futures front-ran the cash session bounce overnight on the same Iran-peace narrative, then carried the move through the open. The longer-dated Treasury complex did the most interesting work — after last week's bond rout sent the 30Y to levels not seen in nearly two decades, today's stabilization gave growth-sensitive contracts (NQ in particular) room to extend gains. For futures traders, the takeaway is that the bond/equity correlation regime is firmly back in "higher yields = lower equities" mode, and any rally that doesn't have yields cooperating is on borrowed time. Pull up the futures dashboard and watch the 10Y like a hawk into Thursday's session.

The Main Event: Nvidia Earnings

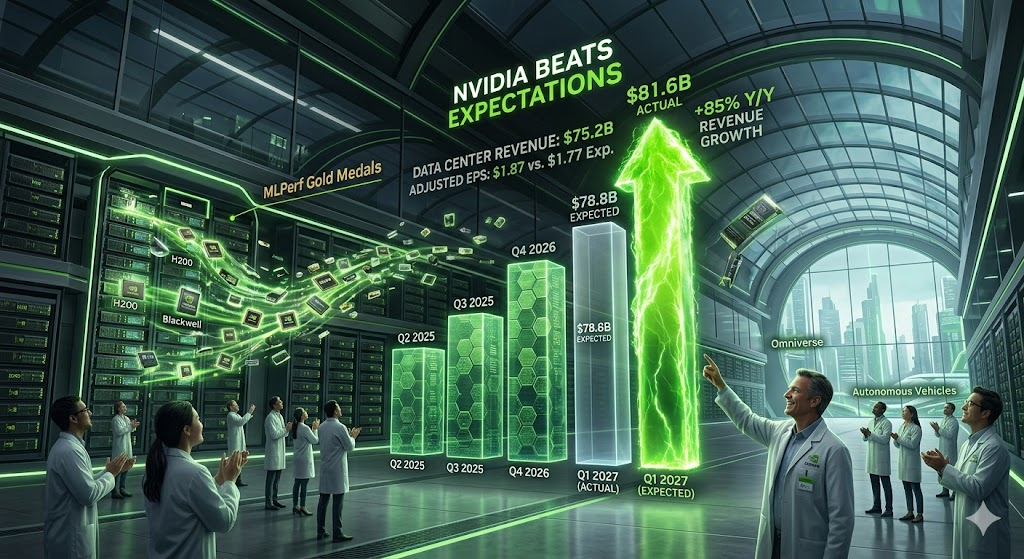

After the close, Nvidia did the thing Nvidia does. Q1 fiscal 2027 results came in at $1.87 EPS on revenue of $81.62 billion, beating consensus of $1.77 and $79.18 billion respectively. Revenue jumped 85% year-over-year from $44.06 billion. The company guided Q2 revenue to $89.1 billion–$92.8 billion against Wall Street expectations of $87.3 billion, authorized $80 billion in additional buybacks, and bumped its quarterly dividend to $0.25 per share from one cent — which is either extreme generosity or extreme accounting humor, depending on how you read it. CEO Jensen Huang offered the now-mandatory quote: "Agentic AI has arrived, doing productive work, generating real value and scaling rapidly across companies and industries," via CNBC.

And the initial reaction? Shares fell more than 2% in the after-hours print. Because nothing rewards a beat-and-raise like a 2% haircut. Options traders had priced in a roughly $355 billion potential market-cap swing — a number that, for context, is larger than the entire market cap of most Fortune 100 companies. The notable footnote: Nvidia is assuming zero data-center compute revenue from China in its outlook, which is either a tell on H20 export restrictions hanging around indefinitely or sandbagging of the highest order. For anyone learning to read these reactions, earnings tape behavior on widely-owned names is a study unto itself — the headline number rarely tells you what the post-print move will be, according to Yahoo Finance.

Crypto: The "We Survived Another Day" Trade

Bitcoin opened at $76,757.31, briefly bounced to $77,428 in early trading, and was changing hands around $77,333 mid-afternoon — up roughly 0.55% on the session. Ethereum followed the same script, opening at $2,110, climbing to $2,128, and settling near $2,133 by midday, up about 0.9%. Solana led the alt complex with a 2.12% gain. The driver is the same one moving every risk asset right now: investors are looking for any sign of a quick resolution to the Iran war, with the Senate having advanced a joint resolution Tuesday aimed at ending the conflict, according to Yahoo Finance.

Zoom out and the picture is uglier. Bitcoin is still down significantly from its October 6, 2025 all-time high of $128,198 — a roughly 40% drawdown that the bulls would prefer you not dwell on. The war, sticky inflation, and rising Treasury yields have been the trifecta from hell for risk assets, and crypto has worn it. The setup into the back half of 2026 is binary: a real ceasefire and a Fed that finally cuts could send BTC back toward the highs, while a renewed escalation or a hawkish September FOMC could test $70K support fast. The crypto tape has effectively become a pure macro proxy at this point, per The Block.

Metals: Gold Catches Its Breath, Silver Tries to Find Itself

Gold has spent the past month getting humiliated. After hitting an all-time high of $5,589 in January, the yellow metal has pulled back roughly 16% as stronger U.S. inflation data reinforced the Fed's higher-for-longer stance and pushed real yields up. Spot gold finished Wednesday around $4,503, up 0.34% on the day — a modest bounce that gold bugs are calling "consolidation" and skeptics are calling "the start of phase two of the correction." Over the past month, gold is down 4.59%, though still 35.65% higher year-over-year. Major institutional forecasters including J.P. Morgan ($5,055 average Q4 2026) and TD Securities ($4,831 annual average, $5,400 highs) continue to see the metal grinding higher into year-end, citing Trading Economics.

Silver has been the more interesting story and the more painful one. After hitting an all-time high of $121.64 on January 29, 2026, the gray metal collapsed through February and March, consolidated in the $70–$80 range, surged 6% on May 11 on the U.S.–China tariff truce, and then got knocked back down by hot April CPI data. Tuesday's session saw silver drop 5% to $73.78 on inflation panic; Wednesday brought a 1.7% rebound to around $75. The gold/silver ratio sits around 55:1, which is below the 60–65 modern average — silver is cheap relative to gold, but that's been true for a while and the market doesn't appear to care. Industrial demand from EVs, AI data centers, and 5G remains the structural bull case, while supply deficits continue stacking up. The trade is real; the timing remains a nightmare, per GoldSilver.

The War, in Two Paragraphs

The 2026 Iran war — initiated by the United States and Israel on February 28 and now nearly three months old — remains the single biggest macro overhang on every asset class. The opening salvo killed Iranian Supreme Leader Ali Khamenei and triggered a retaliatory wave of hundreds of missiles and thousands of drones across the region. Iran's closure of the Strait of Hormuz disrupted roughly 20 million barrels of daily oil supply at its peak, which is how WTI got to $120/bbl in March and is why we're all paying attention to oil tankers again. A patchwork ceasefire has been in effect since April but has been violated by both sides, and Monday saw renewed drone strikes that rattled markets through Tuesday, according to Britannica's reference page.

The latest twist: Trump called off a Tuesday strike on Iran at the request of Gulf allies, told lawmakers he expects the war to end "very quickly," and the Senate is now advancing a bipartisan joint resolution aimed at ending the conflict. Senator Cassidy flipped to support after his primary loss, which is exactly the kind of political development that markets actually trade on. If de-escalation holds, the playbook is straightforward: oil down, yields stabilize, equities and crypto rally, gold consolidates. If it falls apart again — and "again" is the key word given how many times this ceasefire has broken — every one of those moves reverses by Monday morning. Watch the news flow, not your indicators, per Wikipedia's ceasefire timeline.

What's Interesting (Beyond the Numbers)

Three things worth flagging that aren't on the headline tape. First, the bond market is now driving everything. The fact that a session of stable yields produced a 1%+ rally across the indexes tells you that equity multiples are stretched and entirely dependent on the long end behaving itself. Second, Nvidia's decision to assume zero China data-center revenue in guidance is either the most bearish admission about U.S.–China tech relations from any megacap CEO this year, or the cleanest expectation-management setup in the history of guidance. Probably both. Third, OpenAI filing an IPO in the coming weeks at a potential $1T+ valuation would be a generational event — and a meaningful liquidity drain. Pay attention.

Finally, a quiet item that deserves more airtime: India raised its gold import duty from 6% to 15% last week, fully reversing the July 2024 cut. India is the world's second-largest gold consumer, and the duty hike will squeeze affordability for one of the most price-sensitive gold markets on the planet. Local Indian gold prices were already up 60% year-over-year before the duty change. If you're tracking metals fundamentals, that's a real demand-side wrinkle that won't show up in the headlines but will show up in flows, per USAGold's market report.

Setup Into Thursday

Frequently Asked Questions

Why did stocks rally on May 20, 2026?

Equities rallied primarily because Treasury yields stabilized after a multi-day surge, and oil fell on hopes that the Iran war could be nearing resolution. Pre-positioning ahead of Nvidia's after-hours earnings report also contributed to the bid, particularly in the Nasdaq.

Did Nvidia beat earnings expectations for Q1 fiscal 2027?

Yes. Nvidia reported EPS of $1.87 on revenue of $81.62 billion, beating consensus estimates of $1.77 and $79.18 billion. Revenue grew 85% year-over-year, and the company guided Q2 revenue to $89.1B–$92.8B, also above expectations. Shares still initially fell more than 2% after hours.

What is happening with the Iran war and how is it affecting markets?

The U.S.–Israel war on Iran began on February 28, 2026 and has driven a persistent risk premium across oil, gold, and Treasury yields. A patchwork ceasefire is in place but has been violated repeatedly. As of May 20, the Senate is advancing a bipartisan resolution to end the conflict and President Trump has stated he expects it to end "very quickly," which is fueling risk-on flows.

Why did gold and silver sell off in May 2026?

Both metals have pulled back from January highs as hotter-than-expected U.S. inflation data reinforced expectations that the Federal Reserve will hold rates higher for longer. Gold is down roughly 16% from its $5,589 all-time high; silver has fallen sharply from its $121.64 January peak and is consolidating in the $70–$80 range.

Where did bitcoin trade on May 20, 2026?

Bitcoin opened at $76,757 and traded near $77,333 mid-afternoon, up about 0.55% on the day. Ethereum closed near $2,133, up roughly 0.9%. Both remain well below their late-2025 highs, with the macro setup — the Iran war, sticky inflation, and elevated Treasury yields — continuing to weigh on risk assets.

What's the next major catalyst for markets?

Near-term catalysts include Nvidia's stock reaction in Thursday's session, ongoing developments in Iran ceasefire negotiations, Treasury yield movement at the long end, and any further details on OpenAI's reported IPO filing, which Bloomberg says could come "in the coming weeks" at a potential $1 trillion+ valuation.